What is the Corporate Sustainability Reporting Directive (CSRD)?

What is the corporate sustainability reporting directive, otherwise known as the CSRD? Why is it so important for the financial future of the European Union?

Introduced by the European Commission in 2021, the Corporate Sustainability Reporting Directive (CSRD) seeks to standardise non-financial reporting by companies, enhancing the consistency and quality of publicly available data. Notably, these new standards will impact a vast array of organisations, coming into effect on January 1, 2024.

👉 What exactly is the CSRD directive? Who does it concern? What changes can be expected? Why could this directive prove beneficial for your company?

What is the Corporate Sustainability Reporting Directive (CSRD)?

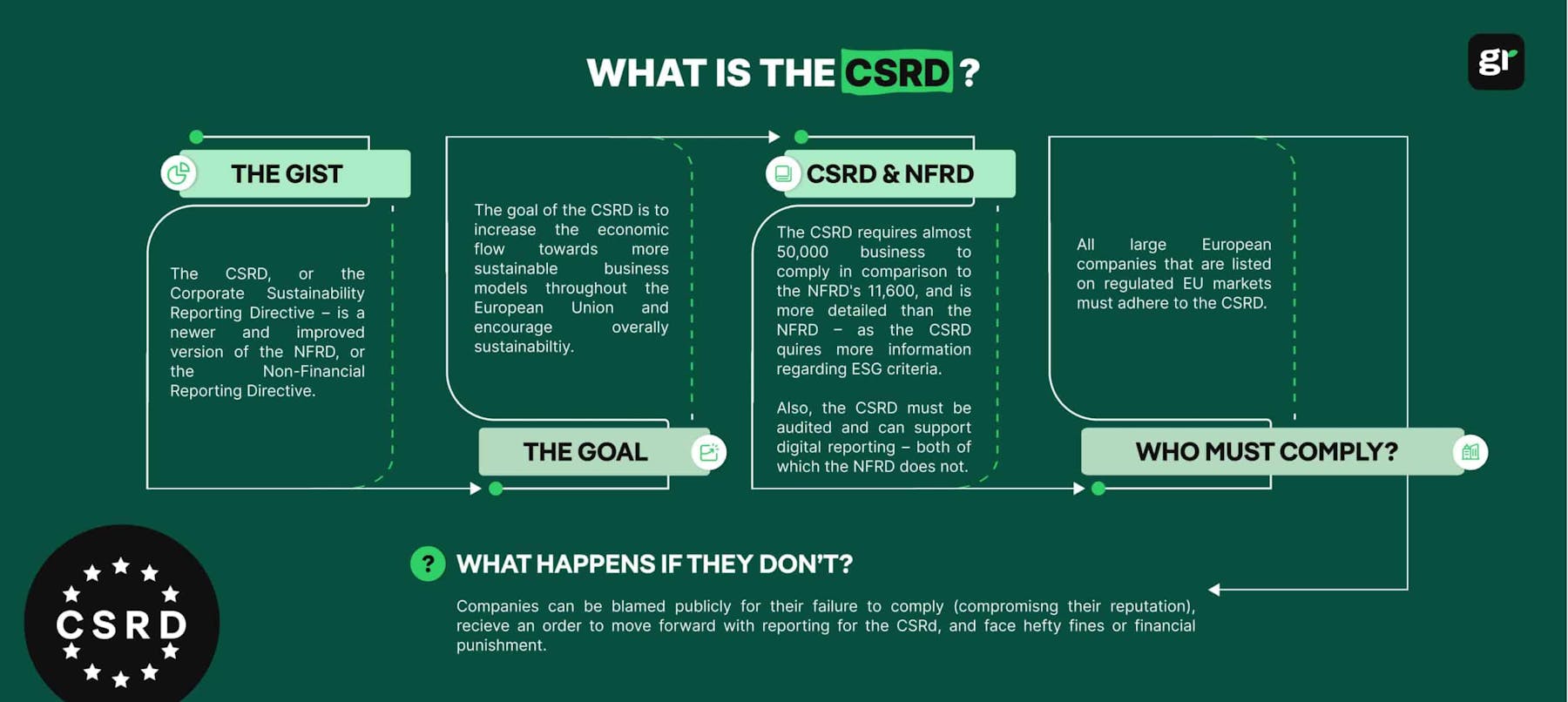

The acronym CSRD stands for Corporate Sustainability Reporting Directive and was drafted by the European Commission in April 2021. This new European regulatory framework for sustainability was published on December 16, 2022, in the Official Journal of the EU.

It will require large companies to publish non-financial reports in accordance with standards established at the European level (the ESRS, which we will discuss further below 👇). Detailed information on risks, opportunities, and material impacts related to social, environmental, and governance issues is expected.

It's important to note that the information needs of financial actors are becoming more and more pressing: let's remember that they are also subject to certain ESG reporting obligations.

Unlike financial reporting, non-financial reporting includes three additional dimensions:

the impact of the activity on the climate;

climate risks weighing on the company;

how the organisation manages these issues.

👉 Until now, the non-financial performance statements of European companies were regulated by the NFRD (Non-Financial Reporting Directive). However, deemed insufficiently ambitious, it will be replaced by the well-known directive (EU) 2022/2464, known as "CSRD"."

Close

What is the main goal of the CSRD?

👉 The main goal of the CSRD is to increase the economic flow towards more sustainable business models throughout the European Union.

Basically, the CSRD aims to accentuate the growing awareness of environmental, social, and governance factors, otherwise known as ESG factors.

It has been shown that most companies do not strive to create transparency and therefore, the European Union feels it is necessary to implement regulations like the CSRD in order to provide companies with the proper incentive to increase their awareness regarding the social and environmental impacts their company may have.

The European Union has always been a leader in environmental measures, and the CSRD helps to unify the European Union in the efforts to cultivate more sustainable business practices.

Who is affected by the CSRD directive?

The CSRD targets financial and non-financial companies covered by the Accounting Directive and the Transparency Directive, and falling into the following categories:

companies listed on European regulated markets, including listed SMEs (micro-enterprises identified by the Accounting Directive are excluded);

other large European companies, listed or not, exceeding two of the three defined thresholds (250 employees, 40 million euros in revenue, and/or 20 million euros in total assets);

non-European companies whose subsidiaries or branches have revenues exceeding 150 million euros within the European Union.

⚠️ Important: If the parent company prepares consolidated reporting, subsidiaries may be exempt from reporting. However, certain information must still be provided by the exempted entity. Furthermore, large listed companies cannot benefit from this arrangement.

Note: SMEs will have reduced reporting obligations. The size of European subsidiaries and branches will also be taken into account. Similarly, non-European companies will only be required to disclose information related to their socio-environmental impacts.

To date, nearly 50,000 companies are identified as being affected by the CSRD directive. While micro-enterprises and non-listed SMEs are not required to publish this report, they can still do so voluntarily.

As a reminder, micro-enterprises are entities meeting the following criteria:

a workforce equal to or less than 10 employees;

a balance sheet equal to or less than 250,000 €;

revenues equal to or less than 700,000 €.

Close

How will the CSRD impact the UK?

The CSRD is taking European countries by storm, as this new directive will require more companies than ever before to disclose their emission activity and other notable environmental impacts – finally requiring the transparency and action in the EU necessary in order to curb climate change once and for all.

However, UK companies may still be in the dark about how the CSRD will affect them – seeing as the CSRD is a European Union initiative to tackle emissions and encourage greater sustainability.

That being said, many companies implicated by the CSRD may have UK counterparts, branches, or partners – meaning that some companies in the UK may be more affected by the CSRD than they might think.

The Corporate Sustainability Reporting Directive (CSRD) could affect companies incorporated in the UK under certain conditions:

EU Market Listings - Companies with securities listed on any EU-regulated market are subject to CSRD obligations, irrespective of their geographical location.

Financial Footprint in the EU - The CSRD applies to companies whose net turnover in the EU exceeds €150 million for the last two consecutive financial years, under either of these circumstances: a) Presence of an EU Subsidiary: A company with an EU subsidiary that either has securities listed on an EU market or is classified as a 'large undertaking.' The latter is defined as a company fulfilling at least two of these criteria: total assets over €20 million, net turnover above €40 million, or an average of 250 employees during the financial year. b) Operations via an EU Branch: A company with an EU branch responsible for a net turnover of more than €40 million in the preceding financial year.

It's crucial for UK-based companies to evaluate their individual situations to see if they are covered by the CSRD. Being subject to CSRD reporting requirements means adhering to its extensive reporting demands and meeting its specified requirements.

UK companies that will be required to report under the CSRD will need to commence preparatory actions for compliance, namely:

Assessing entity eligibility within your group - Start by identifying which entities in your group are based in the EU or have significant business operations there. Evaluate if these entities meet the criteria outlined in the CSRD regulations.

Conduct a comprehensive materiality analysis - Focus your preparations for CSRD compliance by performing a detailed materiality assessment. This step will help pinpoint specific areas where new disclosure requirements will be necessary for your initial reporting period, including policies, key performance indicators (KPIs), and objectives. This approach not only saves time by not focusing on non-material aspects as per CSRD guidelines but also offers valuable insights for your strategic planning.

Evaluate and align disclosure standards - By comparing your current disclosure practices with the new CSRD requirements, you can identify the areas where adjustments are needed. This comparison is key to ensuring your organisation meets the new regulatory standards.

Develop a detailed implementation plan - Once the gaps are identified, create a structured plan outlining how to address them. This includes assigning responsibility within your organisation and discussing the execution strategy with your project team.

What is the timeline for the implementation of the CSRD?

As a reminder, the CSRD was presented to the European Commission and the European Parliament on April 21, 2021. Published on December 16, 2022, in the Official Journal of the EU, it was added to the national legislation of each EU member state by the end of that same year.

The application of this directive will occur on four dates:

January 1, 2025 (for the 2024 fiscal year) for both European and non-European companies already subject to NFRD reporting;

January 1, 2026 (for the 2025 fiscal year) for large European companies and non-European companies listed on a European regulated market not subject to NFRD;

January 1, 2027 (for the 2026 fiscal year) for listed European and non-European SMEs. A small nuance: these SMEs will benefit from an additional two-year extension subject to justification;

January 1, 2028 (for the 2027 fiscal year) for non-European companies whose European revenue exceeds 150 million euros through a subsidiary or branch.

Below is a summary table of the CSRD calendar.

What is the difference between NFRD and CSRD?

The CSRD directive replaces and consolidates the NFRD adopted in 2014, which already aimed to harmonise non-financial reporting.

The main changes to note are:

the digital format becomes mandatory (publication in the unique European electronic format xHTML);

the scope expands (the number of companies subject to reporting increases from 11,600 to nearly 50,000);

the information will be verified by an auditor or an independent organisation;

CSRD reporting now relies on the principle of double materiality (environmental and financial performance become inseparable);

the information will be communicated in a newly dedicated section of the management report.

Good to know: previously, only public interest entities (banks and insurance companies) with more than 500 employees were subject to this form of reporting.

What are the requirements associated with the CSRD?

Compliance with ESRS standards

The ESRS (European Sustainability Reporting Standards) are intended to standardise non-financial statements by companies. The first standards prepared by the EFRAG (European Financial Reporting Advisory Group) were adopted by the European Commission on July 31, 2023.

❗ It's worth noting that in October 2023, the ESRS narrowly escaped being discarded after a majority vote in the European Parliament prevented the standards from being scrapped. The proposal to get rid of the standards stemmed from criticism that the ESRS is lacking in overlap with other disclosure requirements and places too high a burden on businesses.

👉 Two standards specify the general principles and general reporting requirements, while the remaining eleven address the various ESG criteria.

Note: Multiple standards will be gradually adopted (universal, sector-specific, or even specific to SMEs listed on regulated markets).

As a result, all companies will be called upon to pay attention to their social impacts, environmental risks associated with their activity, and their governance practices (pollution, resource use, working conditions, or internal control systems).

👉 To learn more about the ESRS standards and their content, please consult our dedicated article.

consideration of short, medium, and long-term environmental challenges;

treatment of employees and social responsibility;

respect for human rights; combating corruption and bribery;

diversity within boards of directors.

The CSRD adds several requirements applicable from 2023:

risks related to sustainability issues for the company itself;

the impact of the company on the environment;

the announcement of sustainable development goals and measures put in place to achieve them.

Penalties for non-compliance with the CSRD

Sanctions are planned in case of non-compliance with the CSRD. Minimum penalties will have to be defined by each member state.

According to Article 1 of the CSRD, these penalties can take three forms:

a public statement indicating the nature of the infringement and the person concerned;

the issuance of a cessation order related to the area of infringement;

financial sanctions proportional to the profits made through the infringement and the financial strength of the company.

Why was the CSRD created?

1. Establishing a European standard for sustainable development

Through the CSRD, the European Commission creates a regulatory framework and a common language for all economic actors. It serves the objectives set by the EU, which encourages its members to engage in the fight against global warming.

The reporting aligns with the European taxonomy and the regulation governing sustainable finance (SFDR - Sustainable Finance Disclosure). These two mechanisms form an ambitious legislative and regulatory arsenal, aiming to create carbon-neutral finance through so-called "sustainable" investments.

👉 In this sense, the EU continues to encourage companies to implement an effective sustainable development strategy.

2. Clarifying indicators for environmental performance

The CSRD directive is based on the principle of double materiality, which considers both:

the effects of activity on the climate;

the impact of climate change on the activity.

Important: Non-financial reporting must be fed with data that can be compared. The CSRD aims to improve the quality, reliability, and accessibility of information for investors seeking to make evaluations and comparisons.

👉 In this regard, the European Commission has set up a platform (European Single Access Point - ESAP), which centralises all financial and sustainability information.

In practice, this directive will also undoubtedly contribute to combating greenwashing.

Close

What are the 3 actions to take before January 1st, 2025?

Companies already subject to NFRD are already required to report. If you are not one of them, here is how to anticipate the implementation of the evolution of European regulations.

1. Get informed

Let's be honest: the subject is complex. The new rules and requirements induced by the entry into force of the CSRD are numerous, not to mention the host of ESRS standards with which you must become familiar.

Therefore, if your company is concerned about the upcoming changes next year, we urge you to familiarise yourself with these topics as soon as possible.

Our advice: start by familiarising yourself with the fundamentals. Keep in mind that all issues related to the CSRD are related to ESG criteria (Environmental, Social, and Governance). Before looking into the details of your new requirements, make sure you understand the scope of these three concepts - this will be very useful when it comes to defining, collecting, and synthesising the information required.

Then take the necessary time to study the principle of double materiality - a central element of the directive, it will allow you to identify: the main themes to address in terms of opportunities, risks, and impacts; material data representative of these issues (indicators, for example).

👉 EFRAG will shortly publish its guide on "materiality analysis" to support companies subject to the CSRD.

2. Organise

Caution: Producing sustainability reports is not an overnight task. The complexity arises from the numerous functions within your organisation. Ensure you give it the time and attention it deserves.

❗It is important to remember that the implementation of a sustainable development policy involves all levels of the company.

Regarding the implementation of the CSRD, we recommend promptly briefing your teams on this topic. Strategically plan the required steps for your reporting and establish appropriate deadlines.

Vigilance is key: some of the obligations are entirely new. Gathering the necessary information might demand time, and potentially data consolidation too, especially considering the standards encompass the entire value chain.

Yet, it's worth noting that some data might already be at your fingertips. To save time, catalog information shared through various communication channels or under other regulatory guidelines. This ensures you won’t duplicate your efforts!

3. Communicate

Reporting will undergo scrutiny by either an auditor or an independent entity.

In light of this, the directive has expanded the accountability of governance bodies. Essentially, they are tasked with ensuring the accuracy and compliance of the sustainability report presented.

Given the circumstances, we urge affected companies to proactively reach out with any questions to the authorities responsible for upcoming verifications. This proactive approach helps mitigate unforeseen challenges and facilitates necessary adjustments.

Moreover, due to their comprehensive perspective, governance bodies can play a pivotal role in pinpointing the company's key areas of research and analysis. For instance, understanding the climate risks intertwined with the value chain, which includes all company suppliers, can be intricate. Thus, it counts for a substantial part of the work to be done.

👉 CSRD reporting can feel daunting which is why we're here to help! Greenly can guide you all the way through your CSRD reporting, starting with the identification of your disclosure requirements. Our technology and expertise can help you save valuable time through automated data collection and reporting, making the whole process as pain-free as possible. To find out more, head over to our website where you can request a free demo.

Can the CSRD improve worldwide sustainability?

Given the CSRD is only applicable to businesses operating within the EU regulated market and affects European sustainability reporting standards, the directive isn't going to have a direct global impact on sustainability.

However, that isn't to say that the CSRD doesn't hold the potential to influence other nations and regions of the world to require the same sustainability reporting as the European Union does. If the EU can illustrate the environmental benefits of regulations like the CSRD, the world could be well on its way to a more sustainable future.

What about Greenly?

If reading this article about the CSRD, has made you interested in reducing your carbon emissions to further fight against climate change – Greenly can help!

At Greenly, we can help you to assess your company’s carbon footprint, and then give you the tools you need to cut down on emissions. We offer a free demo for you to better understand our platform and all that it has to offer – including assistance with boosting supplier engagement, personalized expertise, and new ways to involve your employees to adhere to all of your reporting requirements such as the CSRD while also going above and beyond in your climate journey.

Learn more about Greenly’s carbon management platform here.

Green-Tok, a newsletter dedicated to climate green news

We share green news once a month (or more if we find interesting things to tell you)

What do Americans think about global warming, how has the U.S. made an effort to reduce greenhouse gas emissions and promote sustainability across the country, and what do Americans do on an everyday basis to fight global warming?

In this article we’ll explore what voluntary carbon markets actually are, how they operate, and the benefits and challenges of their current structure.